Are you planning to buy a house in the near future? Understanding what your credit score is and what factors influence it can give you a confidence boost when buying a home, plus arm you with knowledge if you need to dispute something.

Credit scores are a big factor when buying a home. They are used by mortgage lenders to determine if you’re at risk of defaulting on your loan and even how much they should charge you for the loan. Most consumers don’t really understand what influences their credit score, and even fewer know how lenders calculate the loan pricing. In this blog, we’re going to look at your credit score and the factors that influence it. The more you know, the more you can make a difference.

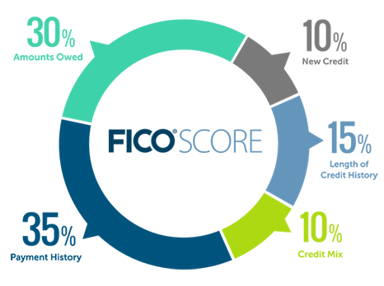

Five primary factors impact your credit score. Can you guess which ones have the most influence? Let’s uncover the facts. We’ll even throw in a few helpful tips…

Length Of Credit History

Length of credit history accounts for only 15% of your credit score. The longer you use credit responsibly, the better your score can be.

Tip: Even if you pay off an older credit card, keep the account open and use it occasionally.

Amounts Owed

The amount you owe on your credit accounts is the second largest contributor to your score. It accounts for 30% of your credit score. The best scenario is low "credit utilization" – using no more than about 20% of the credit available to you.

Tip: If you don't have money to significantly pay down debt right away, consider asking for a higher credit line on an existing account. When you make the request, ask the creditor to make a "soft inquiry" into your credit history, which will not ding your score, rather than a "hard inquiry," which could temporarily cost you some points.

Types of Credit In Use

Types of credit in use accounts for only 10% of your credit score.

It helps your score to maintain a combination of three types of financing: revolving (credit cards), installment (student or personal loans), and secured (auto loans).

Tip: Don't run out and open an account just to have diversity! This is one of the least influential contributing factors.

New Credit

New credit also only accounts for only 10% of your credit score.

Newly established accounts and inquiries for new credit can lower your score. Fortunately, this factor has a relatively small impact.

Tip: Limit the number of new credit inquiries you make and accounts you open, particularly if you're preparing to seek a mortgage or other large loan soon. If you're shopping around for the best deal on new credit, do so in a short amount of time to minimize the impact of multiple queries.

Payment History

Last but certainly not least, pay history accounts for a whopping 35% of your credit score!

The timeliness of your payments is the single biggest contributor to your credit score. It's important not only to make your payments but also to make them by their due dates.

Tip: Have a system in place to assure your bills are always paid on time. Set up automatic withdrawals where appropriate. Keep a cash reserve account to cover payments during possible interruptions to your income.

Bottom Line

Managing your credit is important to obtaining the best terms any time you need to borrow. Best practices may seem counterintuitive, so follow our tips to keep your credit shining. And remember, good habits create good credit. Have questions? Don’t be afraid to reach out to us! We are happy to help.

Helpful Resources

- How can you improve your credit score?

-

How Much Can You Save On Your Mortgage by Improving Your Credit Score?